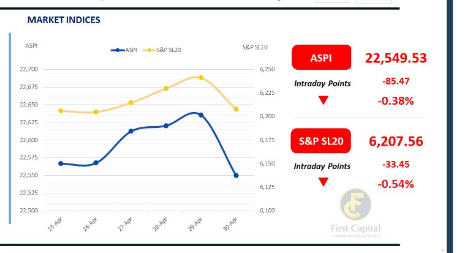

The uncertain global geopolitical environment and the mixed investor sentiment weighed on the market today. The ASPI decreased by 85 points, settled at 22,550, while S&P SL20 closed at 6,208 after losing 33 points.

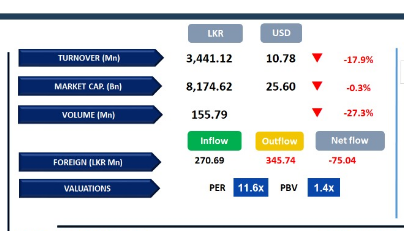

DIAL, JKH, COMB, CCS and MELS emerged as the top negative contributors to the ASPI. HNW investor participation was observed at an elevated level as crossings accounted for 26% of daily turnover.

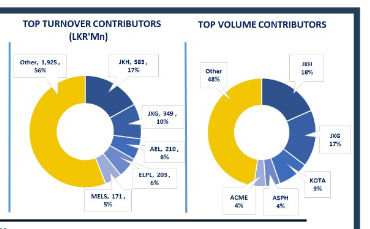

Retail investor participation was observed at an average level. Daily turnover stood at LKR 3.4Bn, marking a decrease of 4.0% over the monthly average of LKR 3.6Bn. Capital Goods sector led the daily turnover with a share of 29%, followed by the Food Beverage & Tobacco, and Diversified Financials sectors collectively contributing 40%. Foreign investors remained net sellers, posting a net outflow of LKR 75.0Mn.

BOND MARKET

Limited activity anchors yield curve

The secondary bond market witnessed subdued trading activity today, with the overall yield curve remaining largely unchanged. Among the maturities traded, the 15.07.2029 bond was quoted at 10.00%, while the 01.07.2030 maturity traded at 10.18%.

Further along the curve, the 15.06.2034 maturity was seen trading in the range of 11.18%-11.21%. Meanwhile, YoY inflation, as measured by the CCPI, rose to 5.4%YoY in April 2026, compared to 2.2%YoY recorded in March 2026. On the external front, the LKR depreciated against the USD, standing at LKR 319.35/USD, compared to LKR 318.69/USD seen yesterday.

Note: Kindly note that the figures relating to excess liquidity and CBSL holdings of government securities for 30th Apr-26 were not available at the time of publication of this document.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..