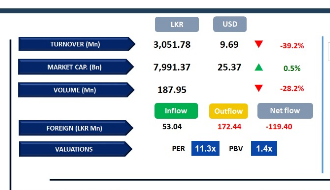

Amid easing oil prices and increasing investor optimism surrounding US-Iran peace talks, the Colombo Bourse concluded today’s session in the positive territory, with the ASPI advancing by 133 points to close at 22,261, while the S&P SL20 edged up by 22 points to settle at 6,175.

JKH, CINS, MELS, HNB, and BREW emerged as the primary positive contributors to the ASPI. Retail investor participation remained elevated, particularly in trading stocks and Hotels sector counters, while HNW investor activity continued to be subdued.

Daily turnover stood at LKR 3.1Bn, marking a decrease of 24.9% over the monthly average of LKR 4.1Bn. Diversified Financials sector led the daily turnover with a share of 26%, followed by Consumer Service, and Capital Goods sectors collectively contributing 32%. Foreign investors remained net sellers, posting a net outflow of LKR 119.4Mn.

BOND MARKET

Soft reopening for secondary market following festive season

Following the festive season, the secondary market reopened with extremely thin trading volumes, leaving the overall yield curve unchanged. Among the maturities that saw activity, the 15.09.2029 bond traded at 10.05%.

Further along the curve, the 01.07.2030 maturity was recorded at 10.15%, while the 15.06.2034 bond traded at 11.15%. At the T-bill auction, weighted average yields edged up across all three tenures with the PDMO partially raising the offered amount of LKR 90.0Bn.

The 3M maturity raised LKR 32.1Bn of the offered LKR 35.0Bn, the 6M maturity raised LKR 17.0Bn of the offered LKR 25.0Bn, while the 12M maturity raised LKR 9.4Bn of the offered LKR 30.0Bn. Weighted average yields moved up to 8.15% (+20bps), 8.22% (+08bps) and 8.52% (+07bps) respectively.

On the external front, the LKR depreciated against the USD, standing at LKR 315.59/USD compared to LKR 315.55/USD seen earlier. Liquidity in the banking system contracted to LKR 105.43Bn from LKR 114.60Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..