Following the announcement of US–Iran peace talks and a temporary ceasefire, easing global oil prices and the broad-based upturn in international capital markets created a favorable environment for equities.

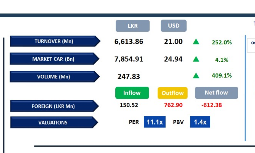

In line with this momentum, the Colombo Bourse concluded the session in positive territory, with the ASPI registering a significant increase of 885 (4.2%) points to close at 21,918.

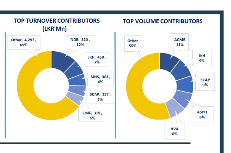

The S&P SL20 index also advanced by 258 points, settling at 6,091. JKH, COMB, HNB, DIAL, and DOCK emerged as the leading positive contributors to the ASPI. Market breadth remained strongly positive, with 246 gainers compared to 16 decliners.

Participation from HNW and retail investors increased notably, reflecting improved investor confidence. Daily turnover stood at LKR 6.6Bn, marking an increase of 62.3% over the monthly average of LKR 4.1Bn.

Banking sector led the daily turnover with a share of 24%, followed by the Capital Goods, and Food Beverage & Tobacco sectors collectively contributing 33%. Foreign investors remained net sellers, posting a net outflow of LKR 612.4Mn.

BOND MARKET

T-bill yields climb briefly at the weekly auction, while the buying sentiment pushed yields down in the secondary market

The secondary market witnessed some buying interest today, following the announcement of US–Iran peace talks and a temporary ceasefire, marking a downward movement in the yield curve.

Among the maturities traded, the 15.06.2029, 15.09.2029 and 15.12.2029 maturities traded between 9.85%-9.70%. 01.03.2030 and 01.10.2032 traded within the ranges of 9.85% - 9.80% and 10.65%-10.58% respectively.

As the yields edged downward in the short-mid-term maturities, 01.06.2033 and 01.11.2033 were dealt between 10.95% and 10.85%. At the T-bill auction, weighted average yields edged up across all three tenures with the PDMO successfully raising the full offered amount of LKR 30.0Bn. All 3M, 6M and 12M maturities were accepted in full, amounting LKR 10.0Bn each.

However, the weighted average yields slightly moved up to 7.95% (+15bps), 8.14% (+05bps) and 8.45% (+04bps) respectively. On the external front, the LKR stayed steady at LKR 315.45/USD compared to previous day. Liquidity in the banking system expanded to LKR 237.26Bn from LKR 225.43Bn recorded previously.

-First Capital Research-

Subscribe to our newsletter to get notification about new updates, information, etc..