Rising geopolitical tensions in the Middle East made both the ASPI and S&P SL20 indices drop sharply lower and stayed in the red, as investors reacted to global uncertainty.

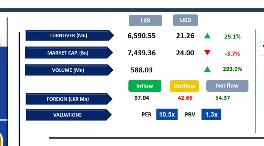

The ASPI declined sharply, closing at 20,939, down 753 points (-3.5%) for the day, falling back into the 20,000 level for the first time since September 2025.

ASPI has now retreated 2,795 points (-11.78%) from its pre-war level of 23,734. S&P SL20 Index closed at 5,885, down 200 points, entering the 5,000 level for the first time since December 2025, and has recorded a cumulative decline of 11.3% from its pre-war level.

Market breadth was negative with 261 counters declining during the session, led by JKH, COMB, HNB, DIAL and DFCC, while only 12 counters showed price gains during the day.

HNW participation remained subdued, while retail activity was elevated amid panic-driven selling. However, the market saw a slight recovery as investors took advantage of bargain-hunting opportunities at discounted price levels.

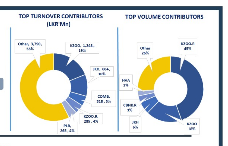

Daily turnover was at LKR 6.6Bn, which is an increase of 26.8% over the monthly average of LKR 5.2Bn. Diversified Financials sector led the daily turnover with a share of 26%, followed by the Capital Goods, and Banking sectors collectively contributing 38%. Foreign investors turned net buyers, posting a net inflow of LKR 54.4Mn.

BOND MARKET

Early-week selling pressure pushes yield curve upward

The week commenced with broad-based selling pressure across all the maturities in the secondary market, amidst limited market activity and low volumes.

The yield curve shifted upwards, following the rise in yields. Over the short-term, 01.07.2028 and 15.12.2028 traded at 9.25% and 9.30% respectively.

Moving ahead, 15.12.2029 traded within a narrow range of 9.65%-9.66%, while 01.03.2030 was seen trading between 9.70%-9.75%.

Further at mid-tenor, 15.03.2031, 01.10.2032, 15.06.2034 and 15.09.2034 changed hands at 9.90%, 10.30%, 10.78% and 10.82% respectively. Finally, the long-dated 15.08.2036 maturity was dealt at 10.87%.

On the external front, the LKR slightly depreciated against the USD, closing at LKR 311.13/USD compared to LKR 311.07/USD recorded the previous day. Liquidity in the banking system contracted to LKR 335.5Bn from LKR 406.8Bn recorded previously.

-First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..