The Colombo Bourse indices showed a mild but steady intraday decline, indicating cautious and slightly bearish sentiment. ASPI is down by 50 points, closing at 23,870, while the S&P SL20 has slipped roughly 7 points to settle at 6,743, with both indices showing early morning strength followed by gradual selling pressure through the afternoon.

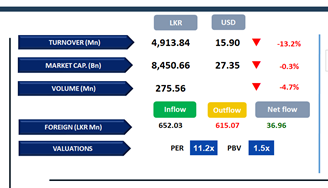

Leading negative contributors to the ASPI were SAMP, DOCK, DIAL, DFCC and COMB. HNW investor participation remained subdued, while retail investor activity was high, particularly in retail trading stocks. Daily turnover stood at LKR 4.9Bn, marking a decrease of 26.9% over the monthly average of LKR 6.7Bn.

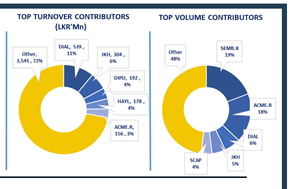

Capital Goods sector led the daily turnover with a share of 21%, followed by the Diversified Financials, and Telecommunication sectors collectively contributing 23%. After 22 days of constant foreign outflows, foreign investors turned to net buyers, posting a net inflow of LKR 37.0Mn.

BOND MARKET

The long end sustains selling pressure, yields edge slightly up

Today the market witnessed some selling activity, particularly at the long end of the curve, which in turn prompted a marginal upward adjustment in the yield curve amid moderate volumes.

At the short end of the yield curve, 15.02.2028, 15.03.2028 and 01.05.2028 traded between 8.98% to 9.05%. Moving ahead, 15.06.2029 traded at 9.40% while 01.03.2030 and 01.07.2030 were seen changing hands at 9.54% and 9.55% respectively. 01.10.2032 maturity was seen trading at 10.25% while 01.06.2033, 15.06.2034 and 15.06.2035 traded at 10.50%,10.70% and 10.80% respectively.

Finally, at the long end of the yield curve, 01.07.2039 was seen changing hands at 10.90%. On the external front, the LKR depreciated against the USD, closing at LKR 309.38/USD compared to LKR 309.32/USD recorded the previous day. Overnight liquidity in the banking system expanded slightly to LKR 283.22Bn from LKR 282.43Bn recorded previously.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..