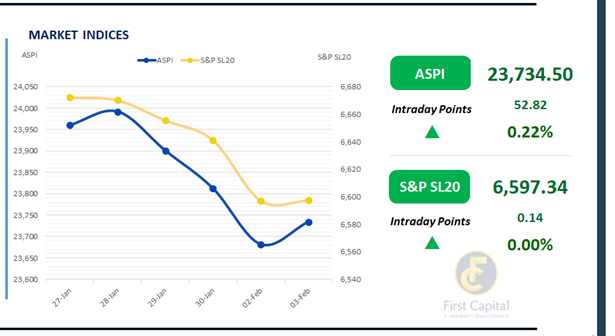

Colombo Bourse moved within a narrow range, showing limited volatility as early gains gave way to consolidation, reflecting cautious and balanced investor sentiment.

ASPI edged up by 53 points to close at 23,735, while the S&P SL20 remained unchanged at 6,597. Top positive contributors to the ASPI were DOCK, TJL, CTC, DFCC and RICH.

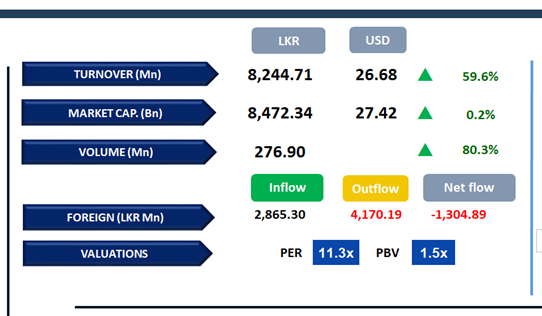

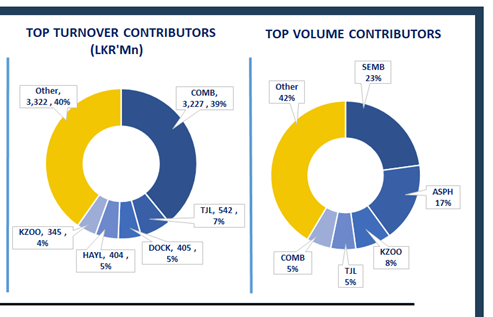

HNW participation was strong, with 49.4% of the day’s total turnover generated through crossings, led by COMB which contributed LKR 3.2Bn (38.9%).

Meanwhile, retail participation remained subdued during the session. Daily turnover stood at LKR 8.2Bn, marking an increase of 17.8% over the monthly average of LKR 7.0Bn.

Banking sector led the daily turnover with a share of 43%, followed by the Capital Goods, and Diversified Financials sectors collectively contributing 26%. Foreign investors continued their sales, posting a net outflow of LKR 1.3Bn, bringing YTD foreign outflows to LKR 8.5Bn.

BOND MARKET

Measured buying persists, volumes improve

Yesterday’s buying interest persisted through today’s trading session while trading activity and overall volumes showed a marked improvement.

Amongst the traded maturities, the 2028 segment, ranging from 15.02.2028 to 15.12.2028 traded between 9.00% to 9.17%.

In terms of 2029 maturities, 15.06.2029 and 15.09.2029 were seen trading between 9.50% to 9.56%. Moving ahead, 01.03.2030 and 15.05.2030 traded at 9.70% while 15.03.2031 and 15.05.2031 were seen changing hands between 9.92% to 10.04%.

Further ahead on the yield curve, 01.06.2033 traded between 10.60% to 10.65% while 15.06.2034 was seen trading at 10.85%.

Finally, the 15.06.2035 maturity, which attracted foreign buying traded at a rate of 10.90%. Today the Public Debt Management Office concluded its weekly T-Bill auction where LKR 89.8Bn was raised against an offer of LKR 120.0Bn.

The weighted average yields inched down across all tenures with that of the 3M Bill inching down by 4bps to settle at 7.80% while that of the 6M and 12M tenures dipped by 9bps and 3bps, settling at 8.17% and 8.33% respectively.

On the external front, the LKR depreciated against the USD, closing at LKR 309.45/USD compared to LKR 309.23/USD recorded the previous day. Overnight liquidity in the banking system expanded to LKR 266.13Bn from LKR 212.55Bn recorded previously.

Courtesy: First Capital Research

Subscribe to our newsletter to get notification about new updates, information, etc..